Bridging the Week by Gary DeWaal

Last week was an abbreviated work week in the United States for many, but it did not stop the Commodity Futures Trading Commission from issuing some report cards to CME Group exchanges, or from the Securities and Exchange Commission from sanctioning two firms each more than US $10 million: one for issues related to the dissemination of equity research and the other for acting in an unregistered capacity. Moreover, an organization of international regulators published a thought piece on issues related to cross-border regulation, and I review Ken Follet’s newest novel, Edge of Eternity.

As a result, the following matters are covered in this week’s Bridging the Week:

- CFTC Issues CME Group Report Card: Scores Generally Good But NYMEX and COMEX Directed to Continue to Enhance Spoofing Surveillance (includes Compliance Weeds);

- IOSCO Consults on Cross-Border Regulation;

- Citigroup Unit Sanctioned US $15 Million by FINRA for Equity Research Dissemination Practices;

- HSBC Swiss Private Banking Unit Fined US $12.5 Million by SEC for Providing Services to US Clients While Being Unregistered;

- Deutsche Bank Sanctioned Almost $200,000 by ICE Futures U.S. for One-Time Speculative Limit Violation; CME Group Fines Three Firms for Documentation Issues Related to EFRPs (includes Compliance Weeds);

- SEC Sues Former Principals of Sanctioned Broker-Dealer for Causing Firm Not to Pay Agreed-Upon Fine;

- Canadian Securities Regulators Propose Adoption of International Standards for Clearing Agencies;

- ISDA Issues Principles for CCP Recovery;

- Follet’s Edge of Eternity Provides Bittersweet Nostalgic Trip Down 60’s and 70’s Memory Lane for Baby Boomers (Totally Irrelevant (But Is It?)); and more.

Video Version:

Article Version:

CFTC Issues CME Group Report Card: Scores Generally Good But NYMEX and COMEX Directed to Continue to Enhance Spoofing Surveillance

The Chicago Mercantile Exchange Group found early presents under its Christmas tree this year in the form of reasonably favorable rule enforcement reviews by the Commodity Futures Trading Commission’s Division of Market Oversight.

CFTC staff examined the enforcement of audit trail requirements by the Chicago Board of Trade and the CME, trade practice requirements by the New York Mercantile Exchange and The Commodity Exchange, and the disciplinary program of all four CME Group entities.

The CFTC staff found that the CME Group exchanges generally complied with all core principles relevant to the specific reviews. CFTC staff recommended, however, that the CBOT and CME design and implement a procedure to “review and enforce” at least annually the exchanges’ process to assign a unique identifier—known as a “Tag 50”—to individual automated trading system operators or teams, and to increase the minimum summary fines relevant to audit trail deficiencies “to defer recidivist behavior;” that NYMEX and COMEX “continue” to enhance their capability to identify spoofing; and that all CME Group exchanges “ensure that internal deliberations do not interfere with the prompt resolution of disciplinary matters.” CFTC staff, in one of the reports, discussed seven matters at CBOT and two at CME that apparently were delayed because of “protracted deliberations” among senior management regarding the exchanges’ pre-hedging rules applicable to block trades.

Just a few weeks ago, CME Group brought and settled over 20 disciplinary actions for payment of fines between US $400 and $5,000 for violations of its requirements related to Tag 50. (Click here for further details in the article “CME Brings Over 20 Disciplinary Actions for Incorrectly Identifying Globex Terminal Operators” in the October 27 to 31 and November 3, 2014 edition of Bridging the Week.)

Compliance Weeds: After the Commodity Futures Trading Commission issued an August 2013 rule enforcement review of CME Group related to its market surveillance and encouraged it to enhance its monitoring of exchange for related positions transactions, CME Group banned transitory EFRPs and brought and settled numerous disciplinary actions involving EFRPs. (Click here to access the article “CME Publicizes a Plethora of EFRP Fines Involving Incomplete Documentation, Late Submissions and Improper Parties,” in the February 24, 2014 edition of what is now known as Between Bridges). Just a few weeks ago, CME Group brought over 20 cases related to Tag 50 infractions—just a short time before the CFTC issued its current report card encouraging CBOT and CME to enhance its summary fines around these identifiers. The CFTC has also asked NYMEX and COMEX to enhance their monitoring of spoofing. Accordingly, it appears timely for trading organizations to update and enforce their internal procedures related to potential disruptive trading practices—if not already done by now. (Click here for details regarding the CME Group’s new rule (Rule 575) prohibiting spoofing and other disruptive trading practices in the article “CME Group Issues New Rule Regarding Disruptive Trading Practices” in the September 4, 2014 edition of Between Bridges.)

IOSCO Consults on Cross-Border Regulation

The International Organization of Securities Commissions published a consultation report discussing different theoretical approaches to cross-border regulation, evaluating such approaches, and ruminating regarding the challenges and opportunities for greater cross-border regulatory cooperation. Analysis in the report derived from an IOSCO member survey from October 2013 to April 2014.

IOSCO is an international body that brings together most of the world’s principal securities regulators. Currently, the organization estimates that its members regulate more than 95% of the world’s securities markets. Its members include over 120 securities regulators and 80 other securities market participants, including exchanges.

In the first instance, IOSCO identified three principal approaches to cross-border regulation: (1) national treatment—meaning the application of applicable rules generally the same to both domestic and foreign persons; (2) recognition—meaning that a domestic regulator relies on a foreign jurisdiction’s regulatory scheme because it assesses that it is “sufficiently comparable; and (3) passporting—meaning that a single jurisdiction’s authorization is satisfactory to permit activities in other jurisdictions.

According to IOSCO, jurisdictions using national treatment do so typically to maintain “a high level of investor protection, maintain market integrity and reduce systemic risks by ensuring that all entities and their activities within a particular market are subject to the direct oversight of the local regulator of that market.” Some survey respondents claimed that this method of regulation helps smaller jurisdictions compete with larger jurisdictions. This is because,

…national treatment does not require the host regulator to conduct an assessment of a regulatory regime that applies to a foreign entity in its home jurisdiction or to issue any type of determination with respect to that regime, there is less of a risk that participants from smaller markets would be excluded by virtue of the fact that authorities would target evaluations of foreign regulatory regimes toward larger and more sophisticated markets which, regardless of any lack of discriminatory intent, could have a discriminatory impact.

Survey respondents using the recognition approach, however, claimed they did so because it improved capital flows and domestic market access to oversee environments; attracted foreign investment to the domestic market; helped ensure adequate investor protection, maintain market integrity and reduce regulatory arbitrage where foreign services, products and market structures were accessible by domestic persons; and enhanced ties with foreign regulators.

The IOSCO survey provided insight into some practical obstacles inhibiting the recognition approach. These included limitations on “human or other resources” necessary to evaluate foreign regulatory regimes; insufficient knowledge and expertise to assess foreign regulatory regimes—particularly when there may be constant changes and language barriers; and regulatory gaps due to differences in basic frameworks and concepts.

Ultimately, claimed IOSCO, the decision on approach will depend on the type of activity and perceived risk; the “robustness and effectiveness” of the foreign regime; and an assessment of the costs and benefits to regulators and markets.

To help promote international cooperation, some survey participants recommended that IOSCO enhance international dialogue between policy makers and regulators in different jurisdictions; provide a “central hub” for information; develop guidelines for assessing different regulatory regimes; and increase the granularity of IOSCO’s own standards and principles, among other measures.

Comments to IOSCO’s consultative report will be accepted through February 23, 2015.

And briefly:

- Citigroup Unit Sanctioned US $15 Million by FINRA for Equity Research Dissemination Practices: Citigroup Global Markets Inc. was fined US $15 million by the Financial Industry Regulatory Authority, principally for supervisory failures relating to its handling of equity research between January 2005 and 2013. According to FINRA, during this time, CGMI equity research analysts engaged in “inappropriate communications” both with external clients as well as internal sales and trading personnel, “including providing non-public research information …before the research was published.” This conduct, claimed FINRA—which was alleged to be a violation of applicable federal securities laws and FIRNA rules—was encouraged by CGMI’s compensation arrangements that rewarded equity research analysts based on feedback from clients and sales personnel. For example, between October 2010 and 2013, equity research analysts occasionally participated in “idea dinners” where they expressed views on stocks inconsistent with their or other CGMI-published research reports. Moreover, when CGMI detected violations of its rules regarding selective dissemination, “it failed to effectively discipline its equity research analysts and therefore failed to adequately enforce its policies and deter future violations,” said FINRA. In addition, claimed FINRA, on two occasions in July 2011, an equity research analyst participated in investment banking roadshows contrary to FINRA requirements. In addition to payment of a fine, CGMI agreed to submit a plan to FINRA within 60 days evaluating its research policies and procedures. CGMI did not admit or deny any of FINRA’s findings. In 2012 and 2013, CGMI agreed to pay two fines totaling US $32 million to the Commonwealth of Massachusetts related to the handling of non-public research information.

- HSBC Swiss Private Banking Unit Penalized US $12.5 Million by SEC for Providing Services to US Clients While Being Unregistered: The Securities and Exchange Commission sanctioned HSBC Private Bank (Suisse) SA US $12.5 million for providing certain broker-dealer and investment advisory services to US persons without registration as a broker-dealer or investment advisor from 2003 through 2011. According to the SEC, these services were provided to approximately 368 permanent US residents for which HSBC realized in excess of US $5.7 million in income. During the relevant time period, charged the SEC, HSBC personnel came to the US to solicit new, or service, existing clients for transactions requiring registration when no registration was effective. Although during the period HSBC “understood there was a risk of violating the federal securities laws by providing broker-dealer and investment advisory services to US clients without being registered with the Commission, and took certain measures to manage and mitigate the risk,” the measures were not sufficiently implemented to prevent the violations, said the SEC. HSBC was fined US $2.6 million and required to disgorge all related net income and to pay prejudgment interest (approximately US $4.2 million) to resolve this matter. HSBC admitted all the facts alleged by the SEC in its order related to this matter, and acknowledged that its conduct violated federal securities laws.

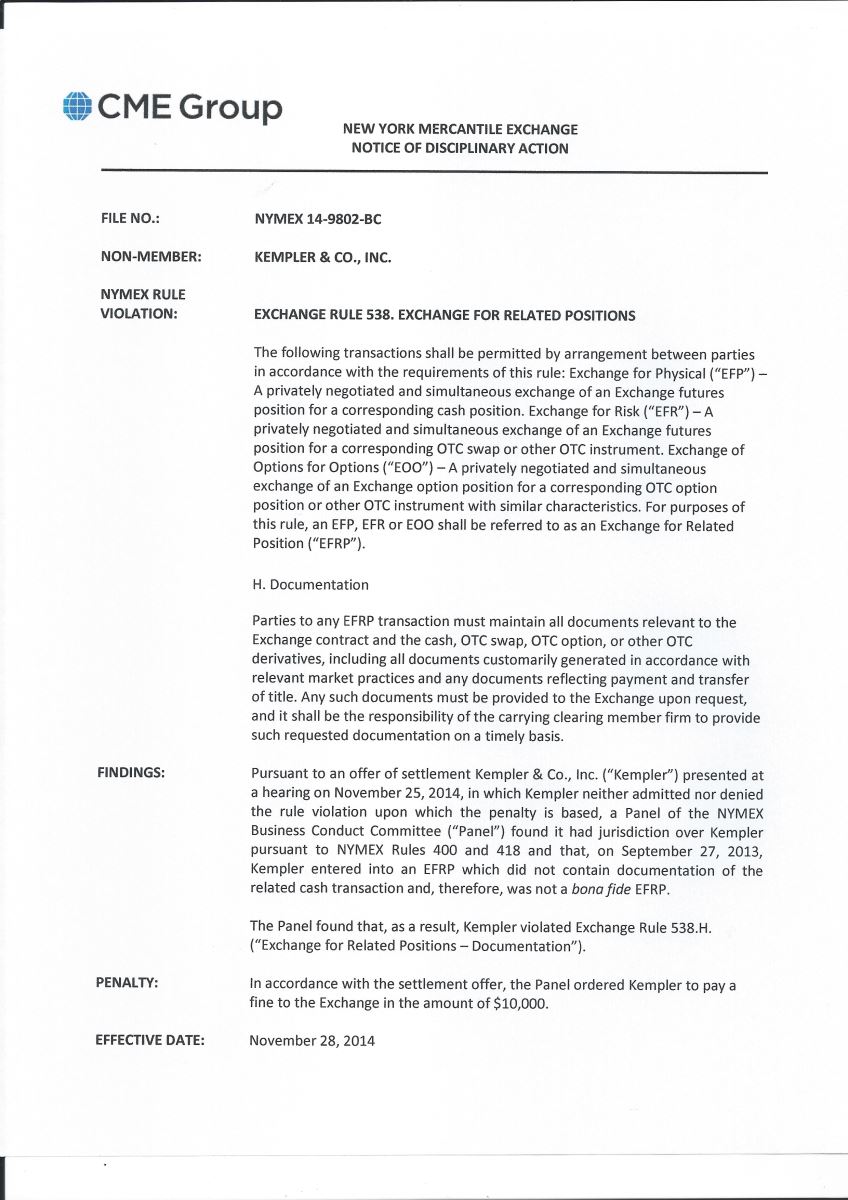

- Deutsche Bank Sanctioned Almost US $200,000 by ICE Futures U.S. for One-Time Speculative Limit Violation; CME Group Fines Three Firms for Documentation Issues Related to EFRPs: Deutsche Bank AG was fined US $20,000 and required to disgorge profits of almost US $175,000 related to a single instance of violating position limits on ICE Futures U.S. According to the exchange, DB exceeded the spot month speculative position limit for the February 2014 contract expiration of the Henry Hub LD1 Fixed Prices futures contract. Separately, CME Group fined one member and two non-members with failing to maintain required documents regarding a single exchange of futures for a related position transaction. In two of the matters—one involving Kempler & Co., Inc., and the other, PFL Futures Limited, both non-members—CME Group found there was no relevant documentation, while in the other—involving Kataman Metals LLC, a member—it found there was insufficient documentation. Kempler and PFL were each fined US $10,000 while Kataman was fined US $15,000.

Compliance Weeds: Repeatedly, exchanges are requiring disgorgement of profits as part of a sanction related to a speculative limit violation. Here the majority of Deutsche Bank’s sanctions by ICE Futures US was repayment of trading profits. This is consistent with a prior action by the same exchange also involving a speculative limit violation earlier this year. (Click here to access the article “ICE Futures U.S. Sanctions Energy Fund for Alleged Position Limit Violations” in the August 11 to 15 and 18, 2014 edition of Bridging the Week.) The Chicago Mercantile Exchange Group has likewise required disgorgement in connection with speculative limit violations. (Click here to access the article “CFTC and CME Bring and Settle Actions for Speculative Position Limit Violations; One CME Action Is for an Intra-day Violation.” In the April 28 to May 2 and May 5, 2014 edition of Bridging the Week.)

- SEC Sues Former Principals of Sanctioned Broker-Dealer for Causing Firm Not to Pay Agreed-Upon Fine: Through an action in a federal court in New Jersey, the Securities and Exchange Commission sought to recover a previously agreed-upon fine against Hold Brothers On-Line Investment Services LLC from the firm’s two principals. Now known as Tafferer Trading, LLC, and alleged to be “likely” dormant, the firm previously was registered as a broker-dealer. According to the SEC’s complaint, Hold Brothers agreed in August 2012 to pay a fine in excess of US $2.5 million in five installment payments over one year to settle a complaint related to manipulative trading practice by traders who used the firm’s electronic trading system. Hold Brothers made one required payment under this agreement for approximately US $500,000. Subsequently, alleged the SEC, rather than pay the fine as agreed, the company paid US $1.4 million in September 2012—the same month the final SEC order related to the fine was issued—to 23 Hold Brothers equity holders. The firm then made no subsequent payments to the SEC on its fine, as required. The SEC alleged that the principals of the firm—Gregory and Steven Hold—directed this payment to shareholders when they were aware of the firm’s obligations to the SEC, and now should be required personally—as so-called “control persons” of Hold Brothers—to pay the remainder of the firm’s fine.

- Canadian Securities Regulators Propose Adoption of International Standards for Clearing Agencies: Canadian securities regulators proposed to adopt international standards as the minimum criteria for clearing agencies to be recognized under applicable Canadian securities laws or to be exempt from recognition (i.e., foreign clearing agencies conducting business in Canada). The international standards are those articulated in the “Principles for Financial Market Infrastructure” adopted by Committee on Payment and Settlement Systems by the Bank of International Settlements in April 2012 (click here to access). The clearing agencies impacted by this proposal are clearinghouses, or central counterparties (so-called “CCPs”), central securities depositories and securities settlement systems. Although there is much parallelism between the proposed Canadian standards and the PFMIs, there are some differences. For example, the Canadian proposal will require Canadian clearinghouses to use a “reasonable portion” of their own capital prior to using the collateral or other prefunded resources of non-defaulting members to cover losses from defaulting participants—a so-called “skin-in-the-game” requirement. According to a notice by the Canadian Securities Administrators, such a requirement “…promotes risk culture and is a positive signal to the clearing agency’s participants that the owners of the CCP have an equal stake in ensuring the robustness of CCP’s risk management.” Comments to the proposal will be accepted through February 10, 2015.

- ISDA Issues Principles for CCP Recovery: The International Securities and Derivatives Association, Inc. issued five “key principles” regarding clearinghouses’ loss-mitigation resources and recovery and resolution. Among other measures, ISDA called for greater transparency regarding clearinghouses’ initial margin methodologies and practices, default fund contributions, and “quantitative disclosures” regarding concentrations to and exposures of individual clearing members so that market participants can better assess potential risks; the implementation of mandatory standardized stress tests to assess clearinghouses’ risk on a consistent basis; the requirement of “material and substantial” skin in the game by all clearinghouses; and the encouragement of clearinghouses’ recovery contingent upon the establishment of “robust” default management plans. ISDA argues that “where [default funds] are not fully prefunded, additional calls to [clearing members] should be pre-defined, limited, quantifiable and fully transparent.”

And even more briefly:

- CFTC Staff Grants CTA Registration Relief to Family Offices Trading for Family Clients: The Commodity Futures Trading Commission Division of Swap Dealer and Intermediary Oversight said it would not require family offices that provide advisory services to family clients to register with the CFTC as a commodity trading advisor. Family offices are typically professional organizations that are wholly owned by clients in a family and exclusively controlled by one or more family members and/or entities controlled by a family. Family offices must file a formal claim with the Division containing certain enumerated information—which is effective upon filing—to take advantage of this relief.

- FIA Updates Guide to Customer Fund Protections: Following the recent implementation of new Commodity Futures Trading Commission rules designed to enhance the protection of customers and customer funds at futures commission merchants and designated clearing organizations, the Futures Industry Association has updated its brochure “Protection of Customer Funds: Frequently Asked Questions.” The brochure describes the segregation regimes for customer funds, where customer funds may be held and invested, and special issues relevant for joint FCMs and broker-dealers, among other topics.

- Treasury Entities Entering Into Swaps for Non-Financial Affiliates Extended Further Relief by CFTC From Swaps Clearing Requirement: Wholly owned treasury affiliates of non-financial companies entering into hedging transactions for non-financial affiliates were granted further relief by the Commodity Futures Trading Commission’s Division of Clearing and Risk from the requirement that certain swaps mandatorily be cleared. Generally, this relief relaxed some of the conditions mandated by the staff’s original relief in June 4, 2013. Reporting counterparties to non-cleared swaps with treasury affiliates taking advantage of this relief have an obligation to report certain enumerated information to a registered swap data repository, or if none is available, to the CFTC in connection with each relevant swap.

- Hong Kong SFC and HKMA Announce Conclusions on Reporting and Record Keeping Related to OTC Derivatives: The Hong Kong Monetary Authority and the Securities and Futures Commission announced a phase-in approach to mandatory reporting and record keeping requirements related to over-the-counter derivatives. In general, such obligations will commence first for authorized institutions, approved money brokers, licensed corporations and clearinghouses, but the requirements for other persons will be deferred. Requirements for asset managers also will be delayed. The first OTC products to be covered will be overnight index swaps while forward rate agreements and foreign exchange derivatives will be covered later.

And finally:

- Totally Irrelevant (But Is It?): Follet’s Edge of Eternity Provides Bittersweet Nostalgic Trip Down 60’s and 70’s Memory Lane for Baby Boomers: I finished reading Ken Follet’s Edge of Eternity just a few days ago. This is supposedly the last in the author’s “Century Trilogy” and provides a cathartic experience for baby boomers, like me, who lived through much of the tumult spanning from the Cuban missile crisis of 1962 and John F. Kennedy’s assassination in 1963, through the 1960’s civil rights movement, the Vietnam war and the anti-war movement, the 1960’s and 1970’s explosion of rock and roll, the 1968 assassinations of Martin Luther King, Jr. and Robert F. Kennedy, and the fall of the Berlin Wall in 1989. Mr. Follet’s specialty is weaving together the lives of fictional characters as they interface with famous historical persons and episodes. His books are dense (The Edge of Eternity is 1098 pages) and sometimes slow plodding, and often the coincidental or purposeful interaction of fictional families from the United States, England, Germany and Russia with each other, let alone with worldwide historical figures, seems too concocted. Notwithstanding, it all works and is worth the ride. In addition, although arguably unfair, Mr. Follet’s integration of oft-repeated rumors (some now reasonably substantiated) regarding the personal lives of some historical features into the fabric of his stories, provides some titillating color. And for those who are younger than baby boomers, this book provides great insight into the times in which their parents grew up and is far more engaging than a traditional history text. For real!

For more information, see:

Canadian Securities Regulators Propose Adoption of International Standards for Clearing Agencies:

http://www.lautorite.qc.ca/files/pdf/reglementation/valeurs-mobilieres/24-102/2014-11-27/2014nov27-24-102-avis-cons-en.pdf

CFTC Issues CME Group Report Card: Scores Generally Good But NYMEX and COMEX Directed to Continue to Enhance Spoofing Surveillance:

http://www.cftc.gov/ucm/groups/public/@iodcms/documents/file/reraudittrail112114.pdf

http://www.cftc.gov/ucm/groups/public/@iodcms/documents/file/rertradepractice112114.pdf

http://www.cftc.gov/ucm/groups/public/@iodcms/documents/file/rerdisciplinaryprogram112114.pdf

CFTC Staff Grants CTA Registration Relief to Family Offices Trading for Family Clients:

http://www.cftc.gov/ucm/groups/public/@lrlettergeneral/documents/letter/14-143.pdf

Citigroup Unit Sanctioned US $15 Million by FINRA for Equity Research Dissemination Practices:

http://disciplinaryactions.finra.org/viewdocument.aspx?DocNB=38038

See also:

Massachusetts 2012 Action:

http://www.sec.state.ma.us/sct/archived/sctciti/Citi_Consent.pdf

Massachusetts 2013 Action:

http://www.sec.state.ma.us/sct/current/sctcitigroup/citigroup-consent-order.pdf

Deutsche Bank Sanctioned Almost $200,000 by ICE Futures U.S. For One-Time Speculative Limit Violation; CME Group Fines Three Firms For Documentation Issues Related to EFRPs:

/ckfinder/userfiles/files/ICE%20Futures%20DN%20Deutsche%20Bank%20AG%202014.jpeg

/ckfinder/userfiles/files/NYMEX%20Kempler%202014(1).jpeg

http://www.cmegroup.com/tools-information/lookups/advisories/disciplinary/COMEX-13-9628-BC-KATAMAN-METALS-LLC.html

http://www.cmegroup.com/tools-information/lookups/advisories/disciplinary/NYMEX-14-9802-BC-PFL-FUTURES-LIMITED.html

{kind=link}

.jpeg){kind=link}

FIA Updates Guide to Customer Fund Protections:

http://www.futuresindustry.org/downloads/PCF_questions.pdf

Hong Kong SFC and HKMA Announce Conclusions on Reporting and Record Keeping Related to OTC Derivatives:

http://www.sfc.hk/edistributionWeb/gateway/EN/consultation/conclusion?refNo=14CP6

HSBC Swiss Private Banking Unit Penalized US $12.5 Million by SEC for Providing Services to US Clients While Being Unregistered:

http://www.sec.gov/litigation/admin/2014/34-73681.pdf

IOSCO Consults on Cross-Border Regulation:

https://www.iosco.org/library/pubdocs/pdf/IOSCOPD466.pdf

ISDA Issues Principles for CCP Recovery:

http://www2.isda.org/news/isda-launches-principles-on-ccp-recovery

SEC Sues Former Principals of Sanctioned Broker-Dealer for Causing Firm Not to Pay Agreed-Upon Fine: http://www.sec.gov/litigation/complaints/2014/comp23143.pdf

Treasury Entities Entering Into Swaps for Non-Financial Affiliates Extended Further Relief by CFTC from Swaps Clearing Requirement:

http://www.cftc.gov/ucm/groups/public/@lrlettergeneral/documents/letter/14-144.pdf

The information in this article is for informational purposes only and is derived from sources believed to be reliable as of November 29, 2014. No representation or warranty is made regarding the accuracy of any statement or information in this article. Also, the information in this article is not intended as a substitute for legal counsel, and is not intended to create, and receipt of it does not constitute, a lawyer-client relationship. The impact of the law for any particular situation depends on a variety of factors; therefore, readers of this article should not act upon any information in the article without seeking professional legal counsel. Katten Muchin Rosenman LLP and/or Gary DeWaal may represent one or more entities mentioned in this article. Quotations attributable to speeches are from published remarks and may not reflect statements actually made.

© 2024 Katten Muchin Rosenman and Gary DeWaal. All Rights Reserved.

Bridging the Week by Gary DeWaal: November 24 to 28 and December 1, 2014 (CME Group Report Cards; Cross-Border Regulation; CCP Recovery; Spec Limits and EFRP Fines; Edge of Eternity)

Block Trades and EFRPs Bridging the Week Compliance Weeds Customer Protection Exchanges and Clearing Houses Managed Money Position Limits Registration Totally Irrelevant (But Is It?)