|

|

For the third week in a row, an enforcement action involving allegations of spoofing was the highlight of financial services industry news. The CFTC brought a lawsuit last week against the same two traders that the CME Group had summarily barred the prior week from accessing all its marketplaces for 60 days for allegedly engaging in disruptive trading earlier this year. Separately, the SEC approved a pilot program to increase the minimum tick size for quotes and trading in certain small capitalization stocks while FinCEN and the US Department of Justice sanctioned two related purveyors of a virtual currency for not maintaining robust AML procedures. As a result, the following matters are covered in this week’s Bridging the Week:

Video Version:

Article Version:

Two Traders Subject of CME Summary Suspension for Alleged Spoofing Sued by CFTC Too

Last week, the Commodity Futures Trading Commission commenced a lawsuit in federal court in New York against Heet Khara and Nasim Salim for alleged spoofing activities on the Commodity Exchange, Inc. from February through at least April 28, 2015. The CFTC claimed the respondents engaged in disruptive trading involving gold and silver futures contracts.

Previously, both respondents were summarily suspended by the CME Group from accessing all its marketplaces for 60 days for the same conduct. (Click here for details in “CME Group Summarily Suspends Trading Privileges of Two Traders Without Hearing for Alleged Spoofing and Non-Cooperation” in the May 3, 2015 edition of Bridging the Week.)

On at least two occasions, alleged the CFTC, Mr. Khara placed multiple small quantity layered orders on one side of the market to help effectuate an execution of a few small quantity orders he previously placed on the opposite side of the market that he desired to be filled. Once some of the desired orders were filled, Mr. Khara cancelled the multiple layered orders on the opposite side of the market.

According to the CFTC, Mr. Khara initially engaged in his disruptive trading practices through an account at an unnamed futures commission merchant (so-called “FCM A”). Mr. Khara’s account was introduced to FCM A by Zonyx DMCC, a Dubai-based unregistered introducing broker that Mr. Salim heads and for which he serves as authorized trader.

After CME Group alerted FCM A on February 25, 2015, regarding certain of Mr. Khara’s alleged disruptive trades and FCM A suspended Mr. Khara’s direct market access, Mr. Khara opened a second account at another unnamed FCM (so-called “FCM B”). Mr. Salim already maintained an account at FCM B.

Afterwards, alleged the CFTC, both Mr. Khara and Mr. Salim individually engaged in similar disruptive trading practices through accounts at FCM B, in the style of Mr. Khara’s prior trading at FCM A. In addition, Mr. Khara and Mr. Salim sometimes coordinated their disruptive trading activities through accounts at FCM B, claimed the CFTC.

In connection with this matter, the CFTC charged Mr. Khara and Mr. Salim with disruptive trading under federal law and CFTC rules, and simultaneously obtained a freeze against all assets of the respondents. The CFTC seeks an injunction, disgorgement of profits and a fine.

Legal Weeds: Unlike in the CFTC’s recently publicized lawsuit against Navinder Sarao for contributing to the May 2010 “Flash Crash” through alleged spoofing activities, the CFTC only alleges against Mr. Khara and Mr. Salim violations of the express prohibition against disruptive trading under federal law and CFTC rules. It does not also allege, as in the CFTC’s case against Mr. Sarao, violations of the prohibitions against manipulation, attempted manipulation and conduct which constitutes a deceptive device or contrivance. (Click here for details in “London-Based Futures Trader Arrested, Sued by CFTC and Criminally Charged With Contributing to the May 2010 ‘Flash Crash’ Through Spoofing” in the April 22, 2015 edition of Between Bridges.) Superficially, there appears to be no material differences in the types of conduct at issue in the two cases, other than Mr. Khara’s and Mr. Salim’s allegedly wrongful conduct occurring during a much shorter time period.

Briefly:

My View: As I wrote just a few weeks ago, although many are now skeptical of virtual currencies, Bitcoin and other cryptocurrencies are receiving more and more attention by investors—both as investments in themselves as well as a commodity around which a nascent support industry is developing. Currently, for example, the Commodity Futures Trading Commission is considering the designation of LedgerX both as a swap execution facility and a derivatives clearing organization in connection with options on Bitcoin. (Click here for details in the article, “LedgerX Seeks CFTC Designation as a Clearinghouse and Swap Execution Facility for Bitcoin Options” in the December 21, 2014 edition of Bridging the Week.) Although there have been issues regarding exchangers of virtual currencies, such as Ripple and XRP LLC, the problems have not been around the integrity of the cryptocurrencies themselves. With enhanced regulation of the purveyors of virtual currencies, it is more likely that cryptocurrency use will become more mainstream. (Click here for an introduction to Bitcoin and an overview of relevant regulatory developments in the November 26, 2013 article “Bitcoin: Current US Regulatory Developments” by Katten Muchin Rosenman.)

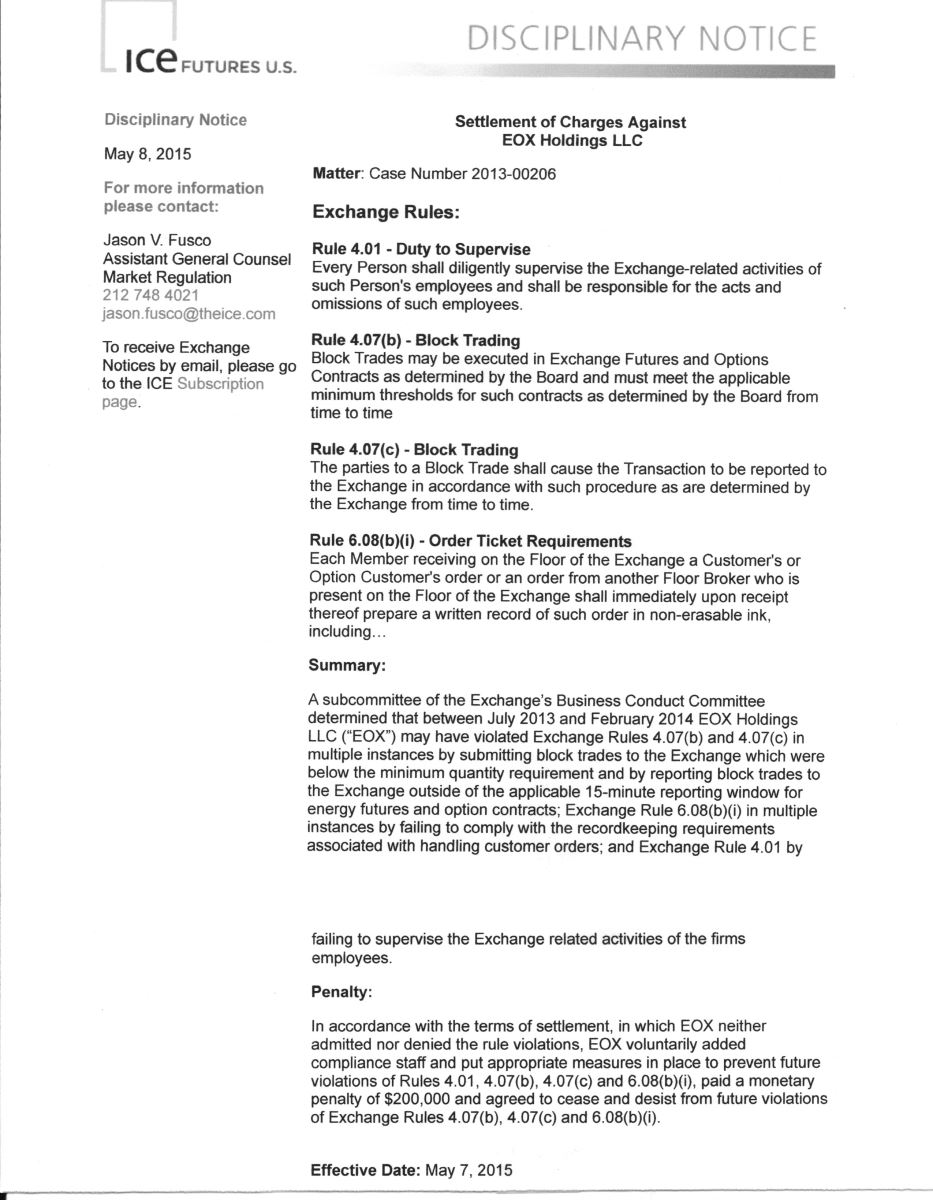

Compliance Weeds: Block trades on ICE Futures U.S. are strictly proscribed (click here to access IFUS Rule 4.07) as clarified, most recently, by an April 24, 2014 FAQ (click here to access). Among other requirements, block trades are subject to minimum thresholds and may only be entered into by so-called eligible contract participants and certain commodity trading advisors; must be executed at prices that are fair and reasonable; are subject to certain recordkeeping requirements; and must be reported within certain time frames. Block trades may only be executed between affiliated entities that have a separate and independent reason to enter into a trade and that are decided by separate and independent decision makers. Parties may not disclose the terms of a block trade to non-involved persons prior to a trade being publicly disclosed. IFUS has a separate prohibition against parties engaging in pre-execution discussions, and taking advantage of such information by trading. (Click here to access IFUS Pre-Execution Communication FAQ, question 3; click here to access “ICE Futures Fines Bank, FCM and Employee US $490,000 for Block Trade Mishandling” in the March 3, 2014 edition of Bridging the Week.)

My View: Ultimately the CFTC and EC will resolve their current debate regarding whether clearing member margin should be based on a two-day or a one-day liquidation period—given the differences in how margin is collected by US clearinghouses (gross basis) and EU clearinghouses (net basis). But there is another requirement for EU clearinghouses that is not currently mandated for US clearinghouses—that EU clearinghouses dedicate at least 25 percent of their capital requirements as skin in the game in their default waterfalls (ESMA had initially considered requiring 50 percent of clearinghouses’ capital requirement but settled at 25 percent; click here to access ESMA’s: “Final Report: Draft Technical Standards under the Regulation (EU) No 648/2012 of the European Parliament on OTC Derivatives, CCPs and Trade Repositories”). When, ultimately, compromises in approach are made to achieve a resolution of the debate whether US clearinghouses are equivalently regulated as EU clearinghouses, it will be interesting to see whether any amendments to approach are adopted in the United States or Europe regarding so-called skin in the game.

And even more briefly:

And finally:

For more information, see:

Broker-Dealer LPL Fined US $10 Million by FINRA for Oversight Failures Related to Complex Products Sales:

http://disciplinaryactions.finra.org/Search/ViewDocument/48016

CFTC Chairman Argues for Equivalent Treatment for US CCPs by the European Commission; EC and CFTC Commit to Continue Talking—That’s All for Now:

Chairman Massad Speech:

http://www.cftc.gov/ucm/groups/public/@newsroom/documents/speechandtestimony/opamassad-20.pdf

Joint CFTC EC Statement:

http://www.cftc.gov/PressRoom/SpeechesTestimony/massadstatement050715

CFTC Commissioner Bowen Says It’s Time to Consider DCO, DCM and SEF Governance:

http://www.cftc.gov/PressRoom/SpeechesTestimony/opabowen-4

Cybersecurity and the Concentration of FCMs Subjects of Upcoming CFTC Market Risk Advisory Committee Meeting:

http://www.cftc.gov/ucm/groups/public/@lrfederalregister/documents/file/2015-10448a.pdf

ESMA Defines Commodity Derivatives to Ensure More Equivalent Application of EMIR:

http://www.esma.europa.eu/system/files/2015-05-06_final_guidelines_c6_and_7.pdf

ESMA and Other European Regulators Warn Risks to EU Financial Market Stability Have Increased:

http://www.esma.europa.eu/system/files/jc_2015_007_jc_report_on_risks_and_vulnerabilities_in_the_eu_financial_system.pdf

ICE Futures U.S. Fines Member US $200,000 for Problematic Block Trades:

/ckfinder/userfiles/files/EOX%20ICE%20Futures%20US.jpeg

IOSCO Consults on Sound Practices to Assess Credit Risk:

https://www.iosco.org/library/pubdocs/pdf/IOSCOPD486.pdf

Money Service Businesses for Second Largest Virtual Currency Fined for AML Deficiencies; Bitcoin Exchange Gets First NY License as Trust Company:

Department of Justice:

http://www.justice.gov/opa/pr/ripple-labs-inc-resolves-criminal-investigation

FinCEN:

http://www.fincen.gov/news_room/nr/pdf/Ripple_Assessment.pdf

http://www.fincen.gov/news_room/nr/pdf/Ripple_Facts.pdf

http://www.fincen.gov/news_room/nr/pdf/Ripple_Remedial_Measures.pdf

New York:

http://www.dfs.ny.gov/about/press2015/pr1505071.htm

Nodal Clear Seeks Designation as CFTC DCO:

http://www.cftc.gov/PressRoom/PressReleases/pr7172-15

See also, Description of Proposed Activities:

http://www.cftc.gov/ucm/groups/public/@otherif/documents/ifdocs/nodalcleardcoappexa-3.pdf

Office of Financial Research Says Concentration of Clearing Imperils CCP Clearing Effectiveness:

http://financialresearch.gov/working-papers/files/OFRwp-2015-07_Hidden-Illiquidity-with-Multiple-Central-Counterparties.pdf

SEC Approves Larger Tick Size Pilot for Small Companies; Study Suggests Larger Tick Sizes May Help HFTs and Not Market Quality:

OFR Report:

http://financialresearch.gov/working-papers/files/OFRwp-2015-08_Systemic-Risk-The-Dynamics-under-Central-Clearing.pdf

SEC Order:

http://www.sec.gov/rules/sro/nms/2015/34-74892.pdf

Two Traders Subject of CME Summary Suspension for Alleged Spoofing Sued by CFTC Too:

http://www.cftc.gov/ucm/groups/public/@lrenforcementactions/documents/legalpleading/enfkharacomplaint050515.pdf

Where to Bring an Enforcement Action: the SEC’s Enforcement Division Issues Guidance Regarding Its Decision-Making:

http://www.sec.gov/divisions/enforce/enforcement-approach-forum-selection-contested-actions.pdf

The information in this article is for informational purposes only and is derived from sources believed to be reliable as of May 9, 2015. No representation or warranty is made regarding the accuracy of any statement or information in this article. Also, the information in this article is not intended as a substitute for legal counsel, and is not intended to create, and receipt of it does not constitute, a lawyer-client relationship. The impact of the law for any particular situation depends on a variety of factors; therefore, readers of this article should not act upon any information in the article without seeking professional legal counsel. Katten Muchin Rosenman LLP may represent one or more entities mentioned in this article. Quotations attributable to speeches are from published remarks and may not reflect statements actually made.

Gary DeWaal is currently Special Counsel with Katten Muchin Rosenman LLP in its New York office focusing on financial services regulatory matters. He provides advisory services and assists with investigations and litigation.

|

Social Media: |

May 03, 2020

April 12, 2020

March 29, 2020

Katten is a firm of first choice for clients seeking sophisticated, high-value legal services in the United States and abroad.

Our nationally recognized practices include corporate, financial services, litigation, real estate, environmental, commercial finance, insolvency and restructuring, intellectual property, and trusts and estates.

Our approximately 650 attorneys serve public and private companies, including nearly half of the Fortune 100, as well as a number of government and nonprofit organizations and individuals.

We provide full-service legal advice from locations across the United States and in London and Shanghai.

Gary DeWaal

Katten Muchin Rosenman LLP

575 Madison Avenue

New York, NY 10022-2585

+1.212.940.6558

{kind=link}

Bridging the Week by Gary DeWaal: May 4 to 8 and 11, 2015 (Spoofing Redux; Virtual Currencies; Larger Tick Size; Block Trades; CCP Equivalency; SEC Forum Choices)

Jump to: AML and Bribery