|

|

Last week was a busy and diverse week of developments in the financial services industry with no one common theme as many aspects were touched by regulators and courts worldwide. In addition, both the chairs of the Commodity Futures Trading Commission and the Securities and Exchange Commission gave some further insights into their priorities, while the European Commission formally delayed implementation of a potentially punitive capital hit for European banks exposed to US clearinghouses. As a result, the following matters are covered in this week’s Bridging the Week:

Video Version:

Article Version:

US Judge Says Sentinel 2007 Transfers to BNY Mellon Cannot Be Reversed as Made in Good Faith

The Bank of New York Mellon Corporation (formerly Bank of New York) was absolved of having engaged in “egregious misconduct” in connection with its relationship with Sentinel Management Group by a United States federal court in Chicago.

Sentinel was an investment management firm registered with the Commodity Futures Trading Commission as a futures commission merchant that claimed it specialized in short-term cash management for hedge funds, individuals, financial institutions and FCMs. The firm filed for bankruptcy in August 2007 after it unlawfully commingled US $460 million of client securities into its house account, and used client collateral to obtain a US $321 million line of credit. Eric Bloom, Sentinel’s former chief executive officer, was convicted earlier this year of defrauding Sentinel’s customers and awaits sentencing.

In August 2013, a US federal appellate court in Chicago had ruled that another proceeding must take place at the lower-level court to determine whether BNY Mellon appropriately protected itself by asserting a lien on assets of Sentinel in connection with a loan it granted the firm. Alternatively, the appellate court sought a determination of whether BNY Mellon was aware that Sentinel was using protected customer assets inappropriately to secure its lien; in which case it must return US $312 million, the value of collateral it held.

In its current decision, the court held that BNY Mellon’s conduct was not sufficiently wrongful to defeat its lien against Sentinel, and that its loan against collateral was made in good faith and should not be avoided. The liquidation trustee of the Sentinel liquidation trust has repeatedly argued that BNY Mellon was obligated to return the collateral to the trust.

Although the court acknowledged evidence that BNY Mellon was aware that Sentinel “was using at least some of the loan proceeds” backed by mixed customer and house collateral “for its own purposes,” the bank believed in good faith that such practice was legitimate, said the court. According to the court, Mr. Bloom, “a Sentinel insider, told [BNY Mellon] that Sentinel had permission, generally, to use client’s segregated funds as collateral for leveraged trading.” The reliance on Mr. Bloom’s representation was reasonable, claimed the court:

Long term stable banking relationships can give rise to actions based, in some part, on trust. That BNYM did not take further steps to investigate Sentinel’s practices for misconduct and, instead, relied on Sentinel’s statements is reasonable in the specific setting of this case. Good faith reliance is an inescapable requisite of a banking finance enterprise. BNYM is neither a father’s keeper nor a partner (despite the current advertising of some banks) of those companies to whom it loans money for business operations. A bank loan is an arm’s length deal. It is both legally and economically wrong to require of a bank the kind of systemic oversight that a parent or holding company often chooses to exercise over a subsidiary. Banks can exercise oversight if they choose, but that oversight is to ensure that the bank’s interest, and not the interest of the debtor, is protected. Close surveillance of the integrity of the debtor and its conduct might be better for a bank, particularly at the outset of the relationship, but this is not an iron-clad duty a bank owes to its debtor or to the debtor’s clients.

In holding for BNY Mellon, the court noted that the National Futures Association had audited Sentinel annually up to 2006, and that McGladrey LLP and its predecessor firm had routinely issued unqualified audit opinions regarding Sentinel’s statement of financial position. Relying on these reviews and the lack of other notice, BNY Mellon was justified in thinking nothing was askew, claimed the court:

There is no evidence in the record that either the auditor or regulator—independent entities with the power of oversight over Sentinel—knew or should have known of wrongdoing before Sentinel’s collapse. BNYM management could fairly rest on the protection of the collateral for its loan at least until such time as the NFA or auditors or, in this case, an inability to honor requests for customer redemptions started the bells ringing. BNYM, I concluded, neither knew nor should have known that Sentinel was misusing loan proceeds or participating in any other misconduct.

(Click here to access further details on the court of appeals decision in the article, “Sentinel Lender Must Face Further Proceedings to Determine Whether Disputed Funds Held Under a Lien Are Owed to Customers” in the October 7 to 11 and 14, 2013 edition of Bridging the Week.)

Appeals Court Sets Aside Insider Trading Convictions Saying Traders Distance From Corporate Insiders Too Far

The convictions of two individuals—Todd Newman and Anthony Chiasson—for insider trading under United States securities law was set aside by a federal appeals court in New York last week.

The court claimed that, in its prosecution of the defendants, the US government failed to demonstrate that the initial insiders from whom defendants’ liability ultimately derived received sufficient personal benefit to establish their (let alone defendants’) securities law liability. Moreover, said the court, the US government failed to provide any evidence that the defendants knew “they were trading on information obtained from insiders in violation of those insiders’ fiduciary duties.”

Mr. Newman—a former portfolio manager at Diamondback Capital Management, LLC—and Mr. Chiasson—a former portfolio manager at Level Global Investors, L.P., were previously charged and convicted of trading in securities based on illegally obtained insider information initially provided by employees at publicly traded technology companies, subsequently shared with analysts at hedge funds and investment firms, and ultimately provided to the defendants. The alleged insider information related to earning announcements of Dell Inc. and Nvidia Corporation prior to the public release of such information in 2008.

The court wrote that three conditions must exist to find criminal liability against an alleged recipient of material non-public information (a so-called “tippee”) for illegal trading on insider information: (1) the corporate insider who was the ultimate source of the information must have had fiduciary duty not to disclose material, nonpublic information; (2) the corporate insider must have breached that duty by disclosing the information to an unauthorized person in exchange for personal benefit; and (3) the tippee alleged to have violated the law must have known or should have known of the breach.

The court concluded that the US government, in its prosecution of defendants, presented insufficient evidence that the corporate insiders received sufficient personal benefit or—even if they did –that defendants knew they were trading on information obtained from persons who had breached their fiduciary duties. Indeed, said the court, "Newman and Chiasson were several steps removed from the corporate insiders and there was no evidence that either was aware of the source of the insider information."

(Click here for further information on this matter in the article, “Second Circuit Clarifies a Heightened Standard for Insider Trading Convictions” in the December 12, 2014 edition of Corporate and Financial Weekly Digest by Katten Muchin Rosenman LLP.)

And briefly:

Compliance Weeds: Both CME Group and ICE Futures U.S. have detailed requirements related to pre-execution communications and minimum required times orders must be exposed to the market prior to crossing. Violations of these requirements could result in enforcement actions both by the exchanges and, in theory, the Commodity Futures Trading Commission (as a violation of its prohibition against non-competitive executions unless undertaken in accordance with rules of an exchange). Click here to access a CME Group cross trade overview, and here to access a recently issued Pre-Execution Communications FAQ by ICE Futures U.S.

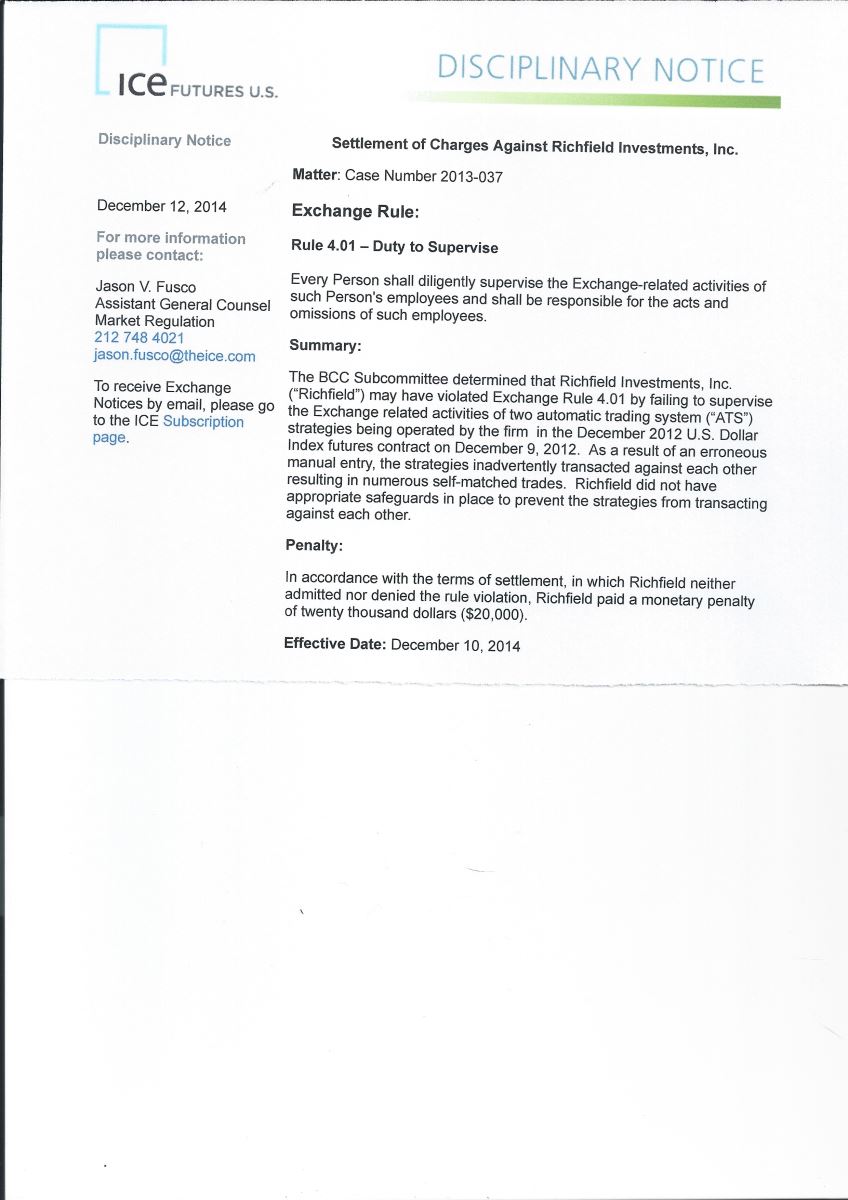

Compliance Weeds: Although futures exchanges may not have per se rules requiring compliance with best practices in relation to automated trading systems, breakdowns can result in enforcement actions under different theories, such as a failure to properly use an exchange’s trading platform (i.e., CME Rule 432W), committing an act which is detrimental to the interest of an exchange (i.e., CME Rule 432Q) or failure to supervise, as in the Richfield Investments matter. Trading firms should also consider employing exchanges’ self trade prevention functionality whether mandated under certain circumstances (such as on ICE Futures U.S.; for more click here) or not (click here for details on CME Group’s capability).

And even more briefly:

For more information, see:

Appeals Court Sets Aside Insider Trading Convictions Saying Traders Distance From Corporate Insiders Too Far:

http://www.ca2.uscourts.gov/decisions/isysquery/3829da65-530d-41f3-aac4-98bdf2149c92/1/doc/13-1837_opn.pdf#xml=http://www.ca2.uscourts.gov/decisions/isysquery/3829da65-530d-41f3-aac4-98bdf2149c92/1/hilite/

Basel Committee Revises Securitization Framework:

http://www.bis.org/bcbs/publ/d303.pdf

…CFTC Chairman Also Sets Forth Priorities to US Senate Committee; Says Individuals Will Be Held Accountable in Enforcement Actions:

http://www.cftc.gov/PressRoom/SpeechesTestimony/opamassad-6#SpTeMBL

Eight Audit Firms Sanctioned by SEC for Providing Both Audit and Non-Audit Services to Audit Clients:

SEC News Release:

http://www.sec.gov/News/PressRelease/Detail/PressRelease/1370543608588#.VIplhb5vl_g

Sample actions:

http://www.sec.gov/litigation/admin/2014/34-73768.pdf

http://www.sec.gov/litigation/admin/2014/34-73773.pdf

European Banks Receive a Stay From Taking Capital Hits for Exposure to US Clearinghouses:

EC Press Release and FAQs:

http://ec.europa.eu/finance/bank/docs/regcapital/acts/implementing/141211-press-release_en.pdf

http://europa.eu/rapid/press-release_MEMO-14-2625_en.htm?locale=en

Implementing Decision:

http://ec.europa.eu/finance/bank/docs/regcapital/acts/implementing/141212-implementing-decision_en.pdf

FINRA Not Playing: Fines 10 Broker-Dealers US $43.5 Million for Research Analyst Violations in Connection With Toys “R” Us Initial Public Offering:

FINRA news release:

http://www.finra.org/Newsroom/NewsReleases/2014/P602059

Sample AWC Decisions:

http://images.magnetmail.net/images/clients/finra/attach/GoldmanSachs_AWC_121114.pdf

http://images.magnetmail.net/images/clients/finra/attach/JPmorgan_AWC_121114.pdf

Firm Fined by ICE Futures U.S. for Not Having Adequate ATS Safeguards to Avoid Self-Matching:

/ckfinder/userfiles/files/ICE%20Richfield.jpeg

See also Disciplinary Notice re: J. Aron:

/ckfinder/userfiles/files/ICE%20J%20Aron.jpeg

First ICE, Then Eurex Announce Swap Futures Contracts:

http://otp.investis.com/clients/us/intercontinental_exchange_group/usn/usnews-story.aspx?cid=953&newsid=22256

http://www.eurexchange.com/exchange-en/about-us/news/Eurex-and-GMEX-cooperate-in-swap-futures-trading-and-clearing/1183910

FXDirectDealer Fined US $500,000 by NFA for AML Violations and Failure to Supervise:

http://www.nfa.futures.org/basicnet/CaseDocument.aspx?seqnum=4058

See also, NFA complaint:

https://www.nfa.futures.org/BasicNet/CaseDocument.aspx?seqnum=4002

ICE Futures U.S. Proposes to Reduce Waiting Time for Execution of Crossing Orders for Certain Contracts:

https://www.theice.com/publicdocs/regulatory_filings/14-127_Admts_to_Pre-Execution_FAQ.pdf

Operator of Non-Registered Securities Trading Venues that Permitted Virtual Currency Payments Fined by SEC:

http://www.sec.gov/litigation/admin/2014/33-9685.pdf

Retail FX Dealer Sanctioned US$ 600,000 by CFTC for Three Days of Net Capital Violations, Failure to Supervise, and Reporting Matter:

http://www.cftc.gov/ucm/groups/public/@lrenforcementactions/documents/legalpleading/enfibfxorderdf121014.pdf

SEC Chairperson Says Commission Will Address Portfolio Composition and Operational Risks by Investment Funds…:

http://www.sec.gov/News/Speech/Detail/Speech/1370543677722#.VIr1cL7qdiE

SEC Okay to Prosecute Cases Before Administrative Tribunals Rather Than Federal Courts Says US Judge:

http://sdnyblog.com/wp-content/uploads/2014/12/14-Civ.-01903-2014.12.11-Opinion-Denying-Preliminary-Injunction.pdf

‘Tis the Season to Give and Receive—But Not Too Much Says the CME Group:

https://www.cmegroup.com/rulebook/files/ra1408-5.pdf

US Judge Says Sentinel 2007 Transfers to BNY Mellon Cannot Be Reversed as Made in Good Faith:

/ckfinder/userfiles/files/BONY%20Sentinel%20December%202014.pdf

…While FINRA Considers Raising $100 Current Gift Limit:

http://www.finra.org/web/groups/industry/@ip/@reg/@guide/documents/industry/p602010.pdf

The information in this article is for informational purposes only and is derived from sources believed to be reliable as of December 13, 2014. No representation or warranty is made regarding the accuracy of any statement or information in this article. Also, the information in this article is not intended as a substitute for legal counsel, and is not intended to create, and receipt of it does not constitute, a lawyer-client relationship. The impact of the law for any particular situation depends on a variety of factors; therefore, readers of this article should not act upon any information in the article without seeking professional legal counsel. Katten Muchin Rosenman LLP and/or Gary DeWaal may represent one or more entities mentioned in this article. Quotations attributable to speeches are from published remarks and may not reflect statements actually made.

Gary DeWaal is currently Special Counsel with Katten Muchin Rosenman LLP in its New York office focusing on financial services regulatory matters. He provides advisory services and assists with investigations and litigation.

|

Social Media: |

May 03, 2020

April 12, 2020

March 29, 2020

Katten is a firm of first choice for clients seeking sophisticated, high-value legal services in the United States and abroad.

Our nationally recognized practices include corporate, financial services, litigation, real estate, environmental, commercial finance, insolvency and restructuring, intellectual property, and trusts and estates.

Our approximately 650 attorneys serve public and private companies, including nearly half of the Fortune 100, as well as a number of government and nonprofit organizations and individuals.

We provide full-service legal advice from locations across the United States and in London and Shanghai.

Gary DeWaal

Katten Muchin Rosenman LLP

575 Madison Avenue

New York, NY 10022-2585

+1.212.940.6558

{kind=link}

{kind=link}

Bridging the Week by Gary DeWaal: December 8 to 12 and 15, 2014 (Insider Trading, Sentinel, Punitive Capital Hit Stay, Investment Funds Portfolio Composition Risk, Auditor Independence (or Not))

Jump to: AML and Bribery