Bridging the Week by Gary DeWaal

The few regulatory and legal developments in the worldwide financial services industry this past week were centered in Europe where a bank, its senior compliance officer and its sole internal auditor were sanctioned for misleading a regulator, while a European court ruled that the European Central Bank could not require all clearinghouses processing euro–denominated transactions to be located solely in the Eurozone as opposed to in the United Kingdom too. A European-based bank was also fined by a US futures exchange for not maintaining required documents to support exchange for related position transactions. As a result, the following matters are covered in this week’s Bridging the Week:

- FCA Sanctions Bank of Beirut, Former Compliance Officer and Former Internal Auditor for Providing Misleading Information Regarding AML Systems and Controls Remediation (includes My View);

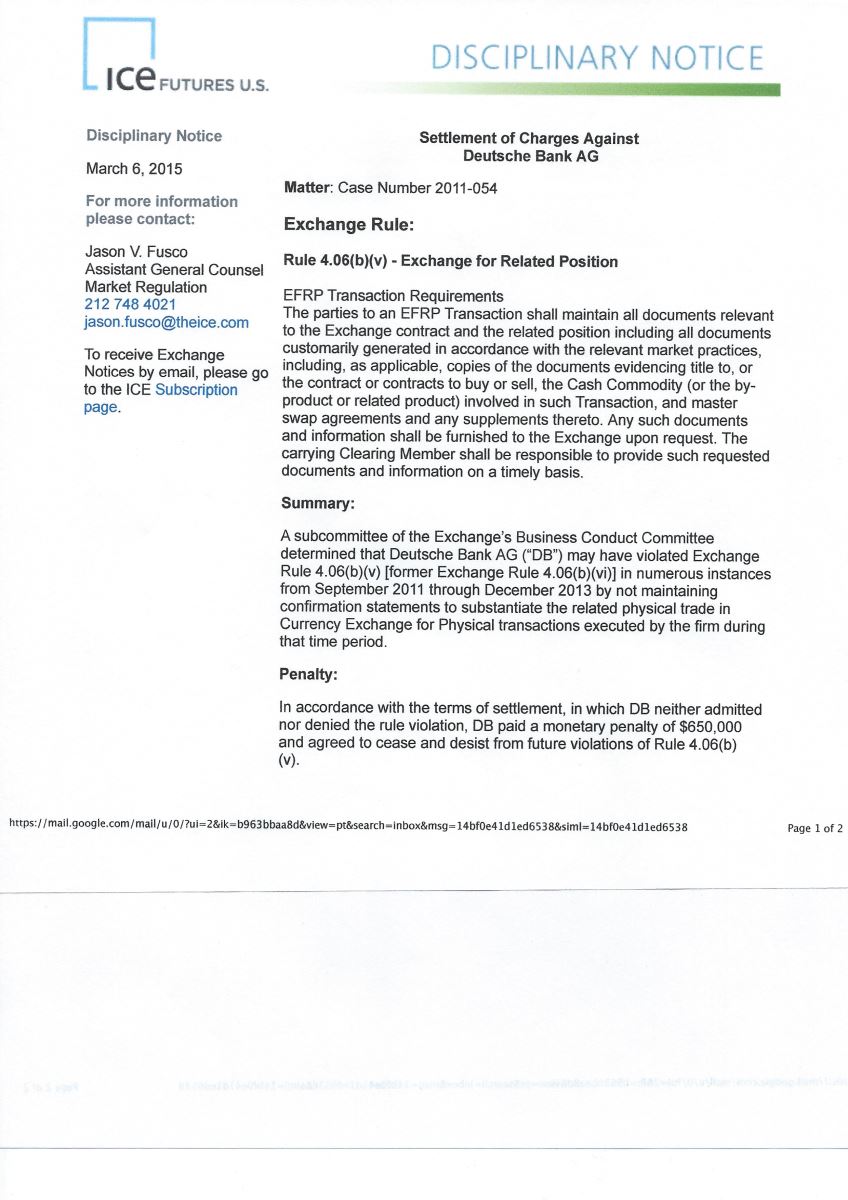

- Deutsche Bank AG Fined $650,000 by IFUS for Documentation Lapses Related to EFRPs (includes Compliance Weeds);

- Broker-Dealer Fined by SEC for Lax Supervision and Violating Customer Protection Rules in Connection With Oversight of Salespersons Who Stole Customer Funds;

- European Court Rules That ECB Wrong to Mandate Clearinghouses Clear Euro-Denominated Trades in Eurozone Only;

- LME Proposes Further Reforms to Reduce Warehouse Delivery Delays; and more.

Video Version:

Article Version:

FCA Sanctions Bank of Beirut, Former Compliance Officer and Former Internal Auditor for Providing Misleading Information Regarding AML Systems and Controls Remediation

The Bank of Beirut was fined GBP 2.1 million (approximately US $3.16 million) by the Financial Conduct Authority for not fixing issues related to its anti-money laundering program in a timely fashion after being told by FCA to address the issues, and for misleading FCA that it had fixed the issues when it had not.

In addition, Anthony Wills, the bank’s former compliance officer (equivalent to a Commodity Futures Trading Commission-regulated chief compliance officer), was fined GPB 19,600 (approximately US $29,500), for providing incorrect information to FCA on a number of occasions, claiming that the bank had completed its requirements to improve its AML program when this was not accurate.

Finally, Michael Allin, the bank’s sole internal auditor, was also fined GBP 9,900 (approximately US $14,900) for preparing writings given to FCA that suggested that the bank had completed its FCA-mandated action points, when it failed to do so. Mr. Allin has been employed in a part-time capacity since January 2012.

Following visits in 2010 and 2011, FCA (including its predecessor, the Financial Services Authority) initially advised the bank to improve its AML program through implementation of a number of “remediation plan action points,” including addressing various AML deficiencies in customer files.

FCA charged that Mr. Wills affirmatively provided FCA incorrect or misleading information “on a number of occasions” when he had an obligation to deal with FCA in an “open and cooperative way and to disclose any information of which FCA would reasonably expect notice.” Indeed, said FCA, it identified one email where Mr. Wills expressly conceded that he had been “fairly guarded” during a conversation with FCA.

Mr. Wills claimed that he had insufficient resources to conduct his role as compliance officer and felt pressured from senior management to be “careful” in his communications with FCA. FCA did not accept this defense:

While the [FCA] recognizes that Mr. Wills’ actions were influenced by comments made by senior management, this does not excuse his misconduct. As Compliance Officer with responsibility for communicating with the [FCA], Mr. Wills’ role at the Bank was particularly significant. Mr. Wills was uniquely placed to understand the full position in relation to Bank of Beirut’s regulatory compliance and as such should have resisted any senior management influence in this regard. As a [regulated] person, he remained personally bound by his own regulatory responsibilities.

In addition to its fine, Bank of Beirut agreed not to open accounts for new customers that are resident or incorporated in high-risk jurisdictions for 126 days.

The FCA has evidenced a penchant among international regulators for naming compliance officers in its enforcement actions. (Click here, for an example, in the article, "Compliance Officers Are in the Cross Hairs Once Again of the UK FCA and the US SEC," in the September 30 to October 4 and October 7, 2013 edition of Bridging the Week.)

My View: Although this matter involving the Bank of Beirut and Mr. Wills was handled by a non-US regulator applying non-US rules, the action may cause pause for chief compliance officers with express, enumerated responsibilities under CFTC rules who wonder what their potential liability might be if something goes wrong at their institution. Among the many responsibilities for CCOs of future commission merchants, swap dealers and major swap participants is “tak[ing] reasonable steps to ensure compliance with the Act and Commission regulations relating to the swap dealer’s or major swap participant’s swaps activities, or to the futures commission merchant’s business as a futures commission merchant.” What this means practically is unclear. However, in adopting its CCO rules, the CFTC expressly rejected industry requests to confirm that the CCO role was solely advisory and suggested that their role is something more. According to the Commission:

[i]n response to comments advocating a purely advisory role for the CCO, the Commission observes that the role of the CCO required under the [Commodity Exchange Act], as amended by the Dodd-Frank Act, goes beyond what has been represented by commenters as the customary and traditional role of a compliance officer. While the Commission does not believe, as some commenters have suggested, that the CCO’s duties under the CEA or [CFTC Rule] § 3.3 requires that the CCO be granted ultimate supervisory authority by a registrant, it is the Commission’s expectation that the CCO will, at a minimum, be afforded supervisory authority over all staff acting at the direction of the CCO. Recent events have demonstrated the importance of the active compliance monitoring duties required of the CCO under the Dodd-Frank Act, as implemented through these regulations.

This is puzzling language at best and leaves CCOs in the United States wondering if they are effective guarantors of their firm’s compliance with laws and rules. It would be helpful for the CFTC to better articulate its expectations for CCOs, considering, again, some of the arguments made by the industry in the lead-up to the adoption of the CCO rules and now the experience of CCOs after a few years. CCOs should ordinarily never be held responsible for the conduct of persons they do not supervise. (Click here to access the CFTC’s discussion of CCO responsibilities in the Federal Register release in connection with adoption of CFTC Rule § 3.3, at pages 20159-20163.)

Briefly:

- Deutsche Bank AG Fined $650,000 by IFUS for Documentation Lapses Related to EFRPs: Deutsche Bank AG agreed to pay a fine of US$ 650,000 to ICE Futures U.S. related to the bank’s apparent failure to maintain confirmation statements to support the physical legs of exchange for related position transactions involving foreign currency. The alleged documentation lapses occurred on “numerous instances” from September 2011 through December 2013, said IFUS. Deutsche Bank neither admitted nor denied any rule violation.

Compliance Weeds: Last year, IFUS, like CME Group before it, updated its rules related to EFRPs and issued a revised “EFRP FAQs.” Among other matters, IFUS’s rules require each of the parties to an EFRP (regardless of whether they are exchange members) to maintain “all documents customarily generated in accordance with the relevant market practice” in connection with the related position. Many firms have been penalized by CME Group and IFUS for failing to prepare and later produce these required documents. (Click here for background on IFUS’s new requirements in the article “ICE Futures U.S. Issues Amendments to Rule and New Frequently Asked Questions Related to EFRPs” in the August 11 to 15 and 18, 2014 edition of Bridging the Week.)

- Broker-Dealer Fined by SEC for Lax Supervision and Violating Customer Protection Rules in Connection With Oversight of Salespersons Who Stole Customer Funds: H.D. Vest Investment Securities, a Securities and Exchange Commission-registered broker-dealer, agreed to pay a fine of US $225,000 to settle charges by the SEC related to the firm’s alleged failure to supervise salespersons who defrauded customers. According to the SEC, HD Vest conducted its business through over 4,500 independent contractor salespersons located in branch offices throughout the United States, the vast majority of whom operated tax businesses utilizing outside business entities. Notwithstanding, HD Vest had no policies and procedures to monitor its salespersons outside businesses. As a result, claimed the SEC, since at least December 2007, an unspecified number of HD Vest salespersons transferred funds from customer accounts or had their customers write investment-related checks to their outside businesses rather than to HD Vest, and subsequently used the funds for personal purposes. HD Vest was also charged with failing, as required by law, to retain all electronic communications with the public, and to set aside adequate funds in a special reserve account for the exclusive benefit of customers. In addition to a fine, HD Vest was required to retain an independent compliance consultant to enhance its supervisory controls. In accepting HD Vest's offer of settlement, the SEC acknowledged the firm's voluntary efforts to improve its AML supervisory systems.

- European Court Rules That ECB Wrong to Mandate Clearinghouses Clear Euro-Denominated Trades in Eurozone Only: In a lawsuit brought by the United Kingdom, the European General Court ruled that the European Central Bank cannot mandate that central clearinghouses that clear euro-denominated trades be located solely in one of the 19 countries where the euro is used as a fiat currency, as opposed to in the UK too. The ECB had implemented such a requirement, arguing that the “negative externalities” that could occur from delays in the settlement of payments if clearinghouses were located outside the Eurozone justified adoption of the requirement. The General Court ruled, however, that the ECB does not have the authority to regulate clearing systems, as its authority only extends to payment systems. The ECB may appeal the court’s decision within two months to the European Court of Justice—the pan-European equivalent of the US Supreme Court for matters related to European law. The General Court is the appellate court below the ECJ. (Click here for further details regarding this decision in the article “European Court Sides with the United Kingdom on Euro Clearing” in the March 6, 2015 edition of Corporate & Financial Weekly Digest by Katten Muchin Rosenman.)

- LME Proposes Further Reforms to Reduce Warehouse Delivery Delays: The London Metal Exchange implemented new rules and proposed new reforms to help ameliorate continued delays in retrieving metals from warehouses and high costs of storage. These are in addition to a new rule (the so-called linked load-in, load-out or LILO rule) implemented on February 1 that required warehouses with delays of more than 50 days for delivering out metal, going forward, to accept less new metal for storage than they deliver out. However, the rollout of these new rules had been delayed by litigation that only recently concluded. (Click here for background on this litigation in the article “UK Court Authorizes LME to Proceed With Reform of Physical Warehouse Network” in the October 6 to 10 and 13, 2014 edition of Bridging the Week.) Among other things, LME proposed to cap or ban charges for storage during periods of long delay (i.e., 50 days or more); proposed refinements to its LILO rule; and provided guidance regarding the types of incentives it considers abusive that warehouse owners may pay to metal owners to attract metal into their warehouses.

And even more briefly:

- Cybersecurity to Be Focus of CFTC Staff Roundtable: Staff of the Commodity Futures Trading Commission will host a roundtable on cybersecurity and system safeguards testing on March 18 at the CFTC’s Washington, DC office. The roundtable principally will address how to enhance the security of futures exchanges, clearinghouses and swap data repositories.

- NFA to Require Swap Dealers and MSPs to Submit Documents to Satisfy Registration Requires Via EasyFile System: Effective today, swap dealers and major swap participants will receive all communications from the National Futures Association related to documents submitted in connection with their registration process in NFA’s Registration Documentation Submission System (RDSS). Going forward, NFA will no longer email communications to firm personnel regarding documents. Instead, it will advise the firm’s chief compliance officer and compliance contact when a new communication is available in RDSS and the firm will be required to view it there.

- US Banks Pass Stress Tests; International Banks Meet Newest Capital Requirements: The Board of Governors of the Federal Reserve System announced that the 31 largest US banks all passed their latest FRB-administered stress tests. These tests projected the impact on the banks’ ratio of high-quality capital to risk-weighted assets from a “severely adverse” economic scenario. Separately, the Bank for International Settlements reported that 224 of the largest international banks now all meet its newest risk-based minimum capital requirements (the so-called Basel III requirements).

For more information, see:

Broker-Dealer Fined by SEC for Lax Supervision and Violating Customer Protection Rules in Connection With Oversight of Salespersons Who Stole Customer Funds:

http://www.sec.gov/litigation/admin/2015/34-74429.pdf

Cybersecurity to Be Focus of CFTC Staff Roundtable:

http://www.cftc.gov/PressRoom/PressReleases/pr7129-15

Deutsche Bank AG Fined $650,000 by IFUS for Documentation Lapses Related to EFRPs:

/ckfinder/userfiles/files/IFUS%20US%20DB.jpeg

{kind=link}

European Court Rules That ECB Wrong to Mandate Clearinghouses Clear Euro-Denominated Trades in Eurozone Only:

Press release:

http://curia.europa.eu/jcms/upload/docs/application/pdf/2015-03/cp150029en.pdf

Decision:

http://curia.europa.eu/juris/document/document.jsf;jsessionid=9ea7d2dc30dd79c902a8ef9140cab624cc10dfad060d.e34KaxiLc3qMb40Rch0SaxuPbhv0?text=&docid=162667&pageIndex=0&doclang=EN&mode=req&dir=&occ=first&part=1&cid=615485

FCA Sanctions Bank, Former Compliance Officer and Former Internal Auditor for Providing Misleading Information Regarding AML System and Controls Remediation:

http://www.fca.org.uk/static/documents/final-notices/bank-of-beirut.pdf

http://www.fca.org.uk/static/documents/final-notices/anthony-rendell-boyd-wills.pdf

http://www.fca.org.uk/static/documents/final-notices/michael-john-allin.pdf

LME Proposes Further Reforms to Reduce Warehouse Delivery Delays:

Overall Update:

https://www.lme.com/en-gb/news-and-events/press-releases/press-releases/2015/03/lme-provides-update-on-warehouse-reform-package/

Detailed Proposal:

https://www.lme.com/~/media/files/notices/2015/2015_03/15%20072%20a071%20w025%20discussion%20paper%20relating%20to%20possible%20reforms%20of%20warehousing%20policy%20and%20physical%20delivery%20network.pdf

NFA to Require Swap Dealers and MSPs to Submit Documents to Satisfy Registration Requires Via EasyFile System:

http://www.nfa.futures.org/news/newsNotice.asp?ArticleID=4549

US Banks Pass Stress Tests; International Banks Meet Newest Capital Requirements:

Basel III:

http://www.bis.org/press/p150303.htm

United States:

http://www.federalreserve.gov/newsevents/press/bcreg/20150305a.htm

The information in this article is for informational purposes only and is derived from sources believed to be reliable as of March 7, 2015. No representation or warranty is made regarding the accuracy of any statement or information in this article. Also, the information in this article is not intended as a substitute for legal counsel, and is not intended to create, and receipt of it does not constitute, a lawyer-client relationship. The impact of the law for any particular situation depends on a variety of factors; therefore, readers of this article should not act upon any information in the article without seeking professional legal counsel. Katten Muchin Rosenman LLP may represent one or more entities mentioned in this article. Quotations attributable to speeches are from published remarks and may not reflect statements actually made.

© 2024 Katten Muchin Rosenman and Gary DeWaal. All Rights Reserved.

Bridging the Week by Gary DeWaal: March 2 to 6 and 9, 2015 (Compliance Officer Sanctioned; EFRPs Redux; Lax Supervision; LME Reform)

Block Trades and EFRPs Bridging the Week Chief Compliance Officers Customer Protection Cybersecurity